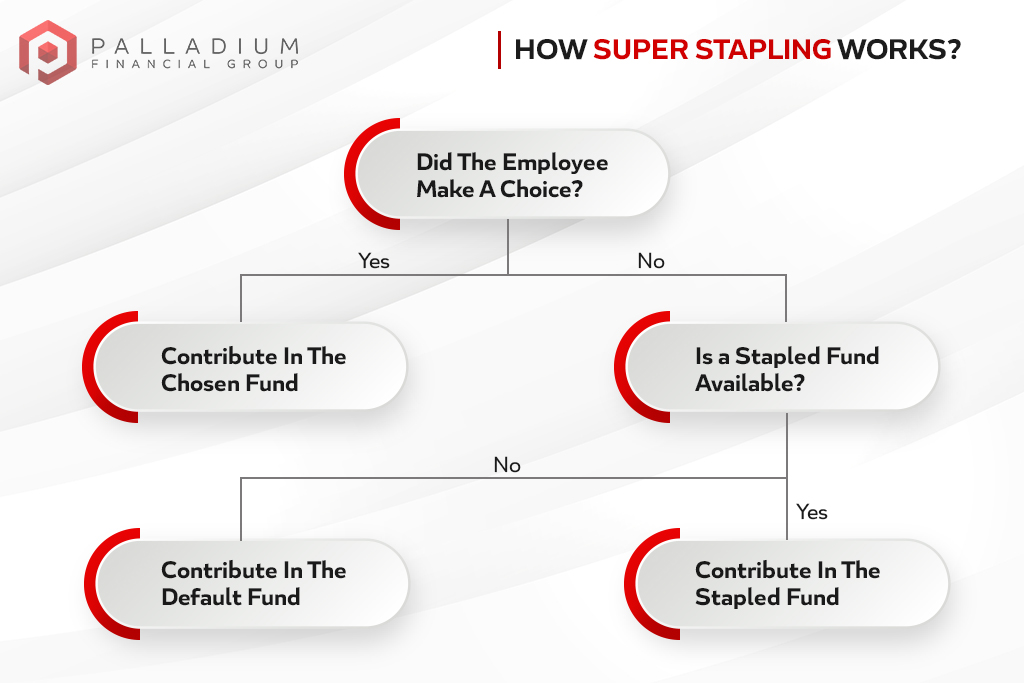

With the introduction of the new rule about stapled super funds, the new Australian employees need to get stapled to their existing super accounts. With the effect of this new law, if an employee does not possess a super fund, it becomes the responsibility of the employer to pay their super contributions in their existing accounts.

A stapled super fund can be referred to as an existing super account stapled to an individual employee and follows them while they are switching their employment. It is introduced and designed by the Government of Australia to stop the practice of possessing multiple super accounts by an employee. Having more than one super account comes along with fees and insurance premiums, making it a costly affair for employees.

There can be chances where a new employee refuses to specify where they want super while commencing a new job. In those conditions, as per the rules, it becomes the employer duty to seek their stapled fund as per the Australian Taxation Office (ATO).

Coming to effect from 1 November 2021, If a new individual joins an organisation, the employer needs to perform one additional step to determine whether you are bound to pay super contributions:

The process of requesting for the stapled fund from the ATO department can be understood by:

1. Employers need to know if they have the optimum access to use the ATO online Services?

2. Log into ATO online services. Enter the employee’s information such as name, date of birth, address and tax file number.

3. Wait for the results to appear (Can take a few minutes).

4. The ATO department will intimate the employee regarding the stapled super fund request and the fund details given by them.

Copyrights © Palladium Financial Group 2026